Risk and Return Dynamics of Top Five Cryptocurrencies: A Comprehensive Analysis using an EGARCH-Based Analysis of Asymmetry and Tail Risk

DOI:

https://doi.org/10.5281/zenodo.17115233Keywords:

Cryptocurrency, Bitcoin, Ethereum, Binance Coin, Tether, XRP, Value at Risk (VaR), Expected Shortfall (ES), Rolling Statistics, Risk Management, EGARCH, Volatility, Skewness, Kurtosis, Financial Risk, Digital AssetsAbstract

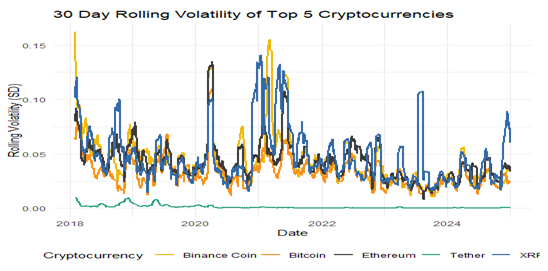

This study examines the risk and returns dynamics of five leading cryptocurrencies—Bitcoin, Ethereum, Binance Coin, Tether, and XRP—over the period from January 2018 to December 2024. Using a combination of traditional and advanced quantitative methods, the analysis incorporates Value at Risk (VaR), Expected Shortfall (ES), and the Exponential Generalised Autoregressive Conditional Heteroskedasticity (EGARCH) model to explore asymmetry and tail behaviour in return distributions. The results show substantial heterogeneity in volatility, risk asymmetry, and persistence, particularly between speculative assets and stablecoins. Tether consistently exhibits low volatility and tail risk, reinforcing its role as a stabilising instrument. EGARCH estimates reveal significant leverage effects in Bitcoin and Ethereum, highlighting the asymmetric impact of negative news on volatility. Rolling-window statistics further capture the time-varying nature of skewness, kurtosis and volatility across assets. These findings provide empirical evidence for the importance of adaptive and asset-specific risk strategies in cryptocurrency markets and contribute to the evolving literature on digital asset risk management.

Downloads

References

Acerbi, C., & Tasche, D. (2002). Expected shortfall: A natural coherent alternative to value at risk. Economic Notes, 31(2), 379–388. https://doi.org/10.1111/1468-0300.00091

Ahelegbey, D. F., Giudici, P., & Mojtahedi, F. (2021). Tail risk measurement in crypto-asset markets. International Review of Financial Analysis, 78, 101957. https://doi.org/10.1016/j.irfa.2021.101957

Alexander, C., & Dakos, M. (2023). Assessing Value-at-Risk and Expected Shortfall using EWMA for cryptocurrency portfolios. Quantitative Finance, 23(2), 299–317. https://doi.org/10.1080/14697688.2022.2159505

Andersen, T. G., Bollerslev, T., Diebold, F. X., & Labys, P. (2003). Modeling and forecasting realised volatility. Econometrica, 71(2), 579–625. https://doi.org/10.1111/1468-0262.00418

Baur, D. G., & Dimpfl, T. (2018). Asymmetric volatility in cryptocurrencies. Economics Letters, 173, 148–151. https://doi.org/10.1016/j.econlet.2018.10.008

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative asset? Journal of International Financial Markets, Institutions and Money, 54, 177–189. https://doi.org/10.1016/j.intfin.2017.12.004

Black, F. (1976). Studies of stock price volatility changes. Proceedings of the 1976 Meetings of the American Statistical Association, Business and Economic Statistics Section, 177–181.

Bouri, E., Lucey, B., & Saeed, T. (2023). Nonlinear dependence and tail risk in cryptocurrency–stock market connectedness. Journal of International Financial Markets, Institutions & Money, 85, 101742. https://doi.org/10.1016/j.intfin.2023.101742

Bruhn, P., & Ernst, D. (2022). A GARCH-EVT-Copula approach to cryptocurrency market risk. Journal of Risk and Financial Management, 15(8), 346. https://doi.org/10.3390/jrfm15080346

Chen, Y., & Chen, M. (2024). Stablecoins and systemic risk: Volatility persistence and contagion dynamics. Journal of Financial Stability, 66, 101281. https://doi.org/10.1016/j.jfs.2024.101281

Cont, R. (2001). Empirical properties of asset returns: Stylised facts and statistical issues. Quantitative Finance, 1(2), 223–236. https://doi.org/10.1080/713665670

Corbet, S., Lucey, B., & Yarovaya, L. (2018). Datestamping the Bitcoin and Ethereum bubbles. Finance Research Letters, 26, 81–88. https://doi.org/10.1016/j.frl.2017.12.006

Corbet, S., Lucey, B., Urquhart, A., & Yarovaya, L. (2019). Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis, 62, 182–199. https://doi.org/10.1016/j.irfa.2018.09.003

Corbet, S., Lucey, B., & Yarovaya, L. (2019). Cryptocurrency and financial stability. Journal of Financial Stability, 39, 168–179. https://doi.org/10.1016/j.jfs.2018.06.006

Dyhrberg, A. H. (2016). Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters, 16, 85–92. https://doi.org/10.1016/j.frl.2015.10.008

Engle, R. F. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation. Econometrica, 50(4), 987–1007. https://doi.org/10.2307/1912773

Feng, W., Wang, Y., & Zhang, Z. (2018). Can cryptocurrencies be a safe haven? A tail risk perspective. Applied Economics, 50(44), 4745–4762. https://doi.org/10.1080/00036846.2018.1466993

Gherghina, Ș. C., & Constantinescu, C. A. (2025). GARCH-type crypto models during geopolitical shocks. Risks, 13(3), 57. https://doi.org/10.3390/risks13030057

Huynh, T. L. D., & Nasir, M. A. (2023). Asymmetric return-volatility transmission in digital currencies: Evidence from EGARCH modeling. Economic Modelling, 124, 106220. https://doi.org/10.1016/j.econmod.2023.106220

Jorion, P. (2007). Value at risk: The new benchmark for managing financial risk. (3rd ed.). McGraw-Hill.

Kar, T., & Meka, S. (2025). Copula-based forecasting of VaR and ES in cryptocurrency markets. Applied Economics. https://doi.org/10.1080/00036846.2025.2476212

Katsiampa, P. (2017). Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters, 158, 3–6. https://doi.org/10.1016/j.econlet.2017.06.023

Kyle, A. S. (1985). Continuous auctions and insider trading. Econometrica, 53(6), 1315–1335. https://doi.org/10.2307/1913210

Liu, J., Zhou, Q., Lin, J., Hao, X., & Chen, Z. (2025). Mean-ES optimisation for crypto markets. Applied Economics. https://doi.org/10.1080/00036846.2025.2503488

Liu, Y., Serletis, A. (2019). Volatility in the cryptocurrency market. Open Economies Review, 30(4), 779–811. https://doi.org/10.1007/s11079-018-9526-8

Liu, Y., Tsyvinski, A., & Wu, X. (2020). Common risk factors in cryptocurrency. NBER Working Paper No. 27707. https://doi.org/10.3386/w27707

Lyons, R. K., & Viswanath-Natraj, G. (2020). What keeps stablecoins stable? NBER Working Paper No. 27136. https://doi.org/10.3386/w27136

Maghyereh, A., & Ziadat, S. A. (2024). Tail-risk transmission in crypto markets during crisis episodes. Financial Innovation, 10(1), 47. https://doi.org/10.1186/s40854-024-00592-1

McNeil, A. J., Frey, R., & Embrechts, P. (2015). Quantitative risk management: Concepts, techniques and tools. (Rev. ed.). Princeton University Press.

Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica, 59(2), 347–370. https://doi.org/10.2307/2938260

Piparo, V. (2025). Backtesting expected shortfall: An application in cryptocurrencies. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5296678

Rehman, S. U., Ahmad, T., & Desheng, W. D. (2024). EGARCH-EVT-Copula risk model for cryptocurrencies. arXiv Preprint. https://arxiv.org/abs/2407.15766

Sapkota, N. (2025). Stablecoin contagion and systemic risk in digital asset markets. Finance Research Letters. https://doi.org/10.1016/j.frl.2025.104789

Trucíos, C. (2019). Volatility forecasting in the Bitcoin market: A comparison of GARCH models. Economics Letters, 174, 118–121. https://doi.org/10.1016/j.econlet.2018.11.015

Trucíos, C., & Siliverstovs, B. (2023). Forecasting cryptocurrency volatility with mixed-data sampling GARCH models. International Review of Financial Analysis, 87, 102549. https://doi.org/10.1016/j.irfa.2023.102549

Wu, C. Y., & Yueh, C. (2025). Volatility transmission and leverage effects in cryptocurrencies: Evidence from EGARCH models. Finance Research Letters, 59, 104556. https://doi.org/10.1016/j.frl.2023.104556

Yousaf, I., & Yarovaya, L. (2023). Spillover and contagion effects among cryptocurrencies and global assets. Finance Research Letters, 54, 103659. https://doi.org/10.1016/j.frl.2023.103659

Zhang, W., & Wang, P. (2022). Tail behaviour and asymmetric volatility in cryptocurrency markets. Journal of Financial Markets, 58, 100651. https://doi.org/10.1016/j.finmar.2021.100651

Zhang, W., Wang, P., Li, X., & Shen, D. (2022). Tail risk and risk spillovers in cryptocurrency markets. Finance Research Letters, 44, 102054. https://doi.org/10.1016/j.frl.2021.102054

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Rahul Biswas

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'International Journal of Engineering and Management Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.