A Bibliometric Analysis on Cryptocurrency Taxation

DOI:

https://doi.org/10.31033/IJEMR/16.2.2026.1893Keywords:

Cryptocurrency, Bitcoin, Blockchain, Tax, Taxation, Digital Currency, Virtual Currency, Crypto Assets, CryptoAbstract

The primary purpose is to trace the progression of scholarly research on cryptocurrency taxation, uncovering prevailing patterns, influential contributors, yearly scientific output and citations, most relevant sources, thematic analysis and cooccurrence networks from 2010 to 2025.

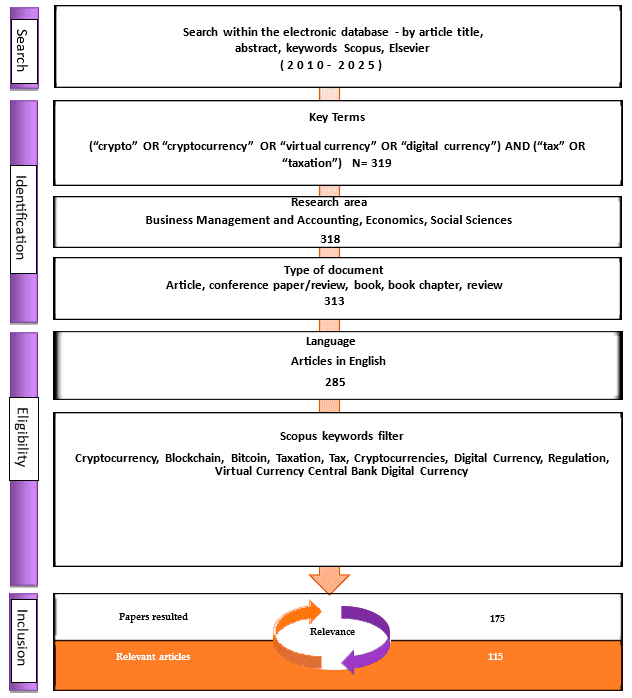

Leveraging a systematic search on Scopus, our final dataset comprises 115 unique documents, with the majority of publications being highly recent (average age of 2.95 years) and exhibiting a robust annual growth rate of 18.65%. The analysis reveals that the field is highly collaborative (average of 2.7 co-authors per paper) and gaining significant scholarly attention, as evidenced by a promising average of 9.548 citations per document. The thematic structure of the literature, mapped through keyword co-occurrence and strategic diagrams, identifies "cryptocurrency," "blockchain," and "bitcoin" as the core, most central themes. The research is highly multidisciplinary, with a strong focus on regulatory, legal, and financial challenges surrounding taxation, anti-money laundering, and the classification of digital assets. While a dominant research source exists, the high dispersion of publications across 85 distinct sources suggests a fragmented but rapidly maturing field.

Downloads

References

Antonopoulos, A. M. (2017). Mastering bitcoin: Programming the open blockchain. (2nd ed.). O'Reilly Media, Inc.

Baur, D. G., & Dimpfl, T. (2021). The volatility of Bitcoin and other cryptocurrencies. In D. G. Baur, & T. Dimpfl (Eds.), Handbook of Blockchain, Digital Finance, and Inclusion, Volume 2: ChinaTech, Mobile Security, and Distributed Ledger (pp. 119-145). Academic Press. https://doi.org/10.1016/B978-0-12-812282-2.00004-8

Hughes, S. J. (2018). Cryptocurrency regulation and taxation. Journal of Financial Crime, 25(3), 670-680. https://doi.org/10.1108/JFC-07-2017-0068

Iansiti, M., & Lakhani, K. R. (2017). The truth about blockchain. Harvard Business Review, 95(1), 118–127.

Kaal, W. A. (2020). Crypto-taxation: A puzzle of inconsistent doctrinal analogies. Wake Forest Journal of Business and Intellectual Property Law, 20(2), 173–216.

Marian, O. (2015). A conceptual framework for the regulation of cryptocurrencies. University of Chicago Law Review Dialogue, 82, pp. 53–72.

Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. https://bitcoin.org/bitcoin.pdf

Organisation for Economic Co-operation and Development (OECD). (2022). Crypto-asset reporting framework and amendments to the common reporting standard. OECD Publishing. https://doi.org/10.1787/492ba036-en

Sharfman, B. S. (2022). The taxation of digitally-native property. Nebraska Law Review, 101(1), 1-46. Retrieved from https://digitalcommons.unl.edu/nlr/vol101/iss1/2

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Anubhav Maurya, Shailesh Kumar Kaushal

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'International Journal of Engineering and Management Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.