Analyzing Financial News Sentiment with NLP to Forecast Market Trends

DOI:

https://doi.org/10.5281/zenodo.13888549Keywords:

Financial Market Sentiment, Social Media Influence, Investor Emotion, BERT Sentiment Analysis, Ensemble Empirical Mode Decomposition (EEMD), Machine Learning, Gold Price ForecastingAbstract

In the era of information explosion, public sentiment, significantly influenced by various information sources including major portals and social media, plays a pivotal role in shaping financial markets. Investor and consumer emotions are highly susceptible to news, rumors, and comments, as exemplified by the "GameStop vs. Wall Street" event where social media influence led to a surge in GameStop's stock value, peaking at $30 billion—over 100 times higher than its value in August. Key social media figures, such as Elon Musk and Donald Trump, can also drastically affect markets with a single tweet, as seen with the Bitcoin and Dogecoin booms following Musk's endorsements.

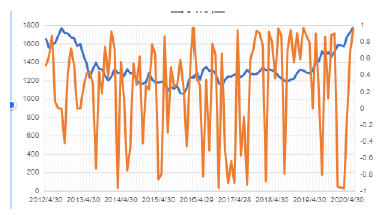

Market sentiment can escalate in cycles of optimism, amplifying positive news and diminishing negative news, or vice versa in periods of pessimism, leading to market despair. This research employs a BERT model for sentiment analysis of financial emotions and integrates Ensemble Empirical Mode Decomposition (EEMD) with machine learning for financial market analysis, including the commodities and stock markets.

The study utilizes the latest data, including monthly (from January 2005 to September 2020) and weekly (from January 7, 2005, to October 2, 2020) gold price data points. The dataset is strategically divided into an 8:2 ratio for training and testing, with 151 monthly data points for training, 38 for testing, and 657 weekly data points for training, alongside 165 for testing. The Mean Absolute Percentage Error (MAPE) is used to gauge the forecasting model's accuracy, a standard metric for assessing predictive model performance.

By integrating EEMD with correlation analysis, this paper aims to elucidate the volatility of gold price closing values and identify the primary drivers of market fluctuations. The robust methodological framework presented enhances the precision of gold price predictions, offering valuable insights for investors and market analysts.

Downloads

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Ziwei Wang, Qian Zhang, Tianzheng Liu, Chao Li

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'International Journal of Engineering and Management Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.