Unveiling the Role of FinTech in Advancing Sustainable Development Goals: A Structural Equation Modeling Approach

DOI:

https://doi.org/10.5281/zenodo.15796067Keywords:

FinTech, Sustainable Development Goals (SDGs), Structural Equation Modeling (SEM), Financial Inclusion, Digital Literacy, Economic Growth, Gender Equality, Climate Action, Education Access, Technological EmpowermentAbstract

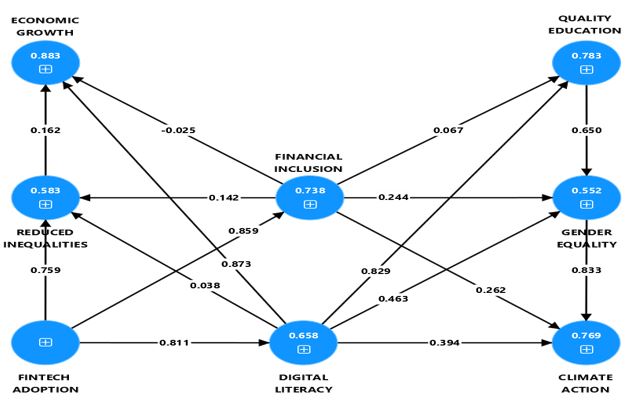

The integration of financial technology (FinTech) into modern economic systems has sparked significant interest regarding its potential to accelerate progress toward the United Nations Sustainable Development Goals (SDGs). This study investigates the structural relationship between FinTech adoption and five selected SDGs—Economic Growth, Quality Education, Gender Equality, Reduced Inequalities, and Climate Action—mediated through Financial Inclusion and Digital Literacy.

Using a Structural Equation Modeling (SEM) framework, we surveyed participants across diverse socio-economic backgrounds to assess how FinTech-driven financial inclusion and digital capability influence sustainable development outcomes. The model reveals that Digital Literacy is the strongest mediating factor, significantly enhancing Economic Growth (β = 0.904), Quality Education (β = 0.829), and Reduced Inequalities (β = 0.859). In contrast, Financial Inclusion plays a more moderate yet targeted role, particularly in addressing inequality and gender-based financial access.

These findings suggest that while FinTech infrastructure is foundational, its real developmental impact is realized through empowerment mechanisms—especially digital literacy. Policymakers and stakeholders are urged to focus on user education and inclusivity when deploying FinTech solutions to ensure alignment with global sustainability objectives.

Downloads

References

D. W. Arner, J. Barberis, & R. P. Buckley. (2017). FinTech and RegTech: Impact on regulators and banks. J. Banking Regulation, 19(3), 1–14.

P. Gomber, J.-A. Koch, & M. Siering. (2017). Digital finance and FinTech: Current research and future research directions. J. Business Economics, 87, 537–580.

D. A. Zetzsche, R. P. Buckley, D. W. Arner, & J. N. Barberis. (2017). From FinTech to TechFin: The regulatory challenges of data-driven finance. Univ. Hong Kong Faculty of Law Res. Paper, No. 2017/007.

United Nations. (2015). Transforming our world: The 2030 agenda for sustainable development. Available at: https://sdgs.un.org/2030agenda.

UNDP. (2020). FinTech and the SDGs: Leveraging financial technology for inclusive development. United Nations Development Programme.

World Economic Forum. (2019). The role of financial innovation in achieving the SDGs.

A. Klein. (2020). Can FinTech address financial inclusion and the SDGs?. Brookings Institution.

A. Demirgüç-Kunt et al. (2022). The global findex database 2021: Financial inclusion, digital payments, and resilience in the age of covid-19. Washington, DC: World Bank.

W. Jack, & T. Suri. (2014). Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. American Economic Review, 104(1), 183–223.

T. Suri, & W. Jack. 92016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288–1292.

G. Chen, & S. Rasmussen. (2014). Digital financial services: Challenges and opportunities. CGAP Brief.

UNESCO. (2018). A global framework of reference on digital literacy skills for Indicator 4.4.2.

OECD. (2016). Skills for a digital world. OECD Science, Technology and Industry Policy Papers, No. 41.

GSMA. (2022). The mobile gender gap report 2022. GSM Association.

J. F. Hair, W. C. Black, B. J. Babin, & R. E. Anderson. (2010). Multivariate data analysis. (7th ed.). Pearson.

B. M. Byrne. (2016). Structural equation modeling with AMOS: Basic concepts, applications, and programming. (3rd ed.). New York: Routledge.

World Bank. (2022). World development indicators: Economic growth and innovation. Available at: https://databank.worldbank.org.

United Nations Statistics Division. (2022). SDG global indicators database. Available at: https://unstats.un.org/sdgs/indicators/database/.

S. Claessens. (2004). Regulation and supervision of financial intermediaries in emerging markets: An overview. World Bank Res. Obs., 19(1), 1–23.

E. J. McGuire. (2019). Digital identity: Fundamental enabler of FinTech and inclusive growth. J. Financial Innovation, 5(2), 112–128.

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Yogita Madhukar Patil, Namit Bhatnagar, Shourya Banarjee

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'International Journal of Engineering and Management Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.