Analyzing the Impact of Systematic Risk, Market Capitalization and Firm Size on the Financial Performance of Selected Companies Listed in SENSEX

DOI:

https://doi.org/10.31033/IJEMR/16.1.2026.1853Keywords:

Financial Performance, Systematic Risk, Market Valuation, Firm Size, Price to Book Value RatioAbstract

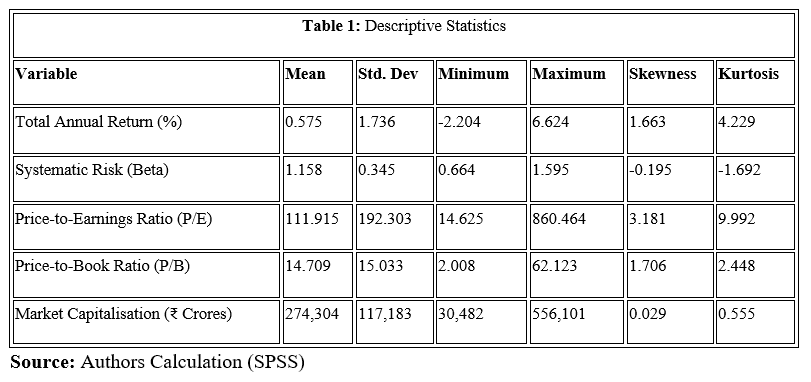

Our Study evaluates that the impact of systematic risk, market valuation and firm size on the financial performance of selected Sensex companies. The objective of our study is to identify which factors most strongly influence annual stock returns and provide direction for investors and portfolio managers. In our study, data collected from 25 companies over the period 2021–2025 were analyzed using descriptive statistics, normality tests, correlation, regression and ANOVA analysis test. Descriptive analysis showed variation in total returns, risk measures and market valuation indicators. Normality tests confirmed the data distribution was suitable for further statistical analysis. Correlation results indicated weak to moderate relationships between financial performance and independent variables. Another statistical tool that is Regression analysis highlighted that firm size which is measured by market capitalization, has a significant negative effect on total annual return, whereas systematic risk, price-to-earnings ratio, and price-to-book value ratio were not significant predictors. ANOVA stated that there was no significant differences in returns across financial years, suggesting relative stability over time. In our study the findings suggest that firm size is a key determinant of stock performance in the Indian equity market. This study provides empirical evidence that can assist investors and portfolio managers in making informed decisions and prioritizing firm size when evaluating stock returns.

Downloads

References

Anwar, M., & Kumar, S. (2018). Testing the capital asset pricing model in Indian stock market. Indian Journal of Research in Capital Markets, 5(4), 38–52. https://indianjournalofcapitalmarkets.com/index.php/ijrcm/article/view/141546/0

Arathi, R., & D’Souza, S. (2023). Risk and return evaluation on BSE SENSEX stocks. International Journal of Commerce and Management Research, 9(6), 67–70. https://www.managejournal.com/assets/archives/2023/vol9issue6/9147.pdf

Farhana, N., & Azees, S. (2025). Testing CAPM and beta dynamics in the Indian stock market. Journal of Informatics Education and Research, 5(3). https://jier.org/index.php/journal/article/view/3310

Rabha, T., Singh, R., & Vanlalzawna, H. (2025). Size, value, and market risk factors in Indian equity markets: Evidence from the Fama–French framework. Indian Journal of Research Capital Markets, 12(2). https://indianjournalofcapitalmarkets.com/index.php/ijrcm/article/view/175458

Sharma, N., Bhargava, P., & Sunail, R. (2024). Risk and return relationship: A study of BSE Sensex stocks in Indian stock market. Journal of Technology Management for Growing Economies, 15(1), 41–61. https://tmg.chitkara.edu.in/2024/risk-and-return-relationship-a-study-of-bse-sensex-stocks-in-indian-stock-market

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Sandip Bhattacharyya, Vinay Kumar Shaw

This work is licensed under a Creative Commons Attribution 4.0 International License.

Research Articles in 'International Journal of Engineering and Management Research' are Open Access articles published under the Creative Commons CC BY License Creative Commons Attribution 4.0 International License http://creativecommons.org/licenses/by/4.0/. This license allows you to share – copy and redistribute the material in any medium or format. Adapt – remix, transform, and build upon the material for any purpose, even commercially.