On A Python-based Extensible Factor Analysis Platform with Quantile Regression Capability for Evaluating Stock Selection Strategies

DOI:

https://doi.org/10.5281/zenodo.12703936Keywords:

Quantitative Trading, Backtesting, Factor Analysis, Quantile Regression, CythonAbstract

Factor analysis selects stocks by studying which factors affect stock returns significantly. However, the amount of stocks to be purchased based on the selected factors is usually important but not well-considered in factor analysis. Quantile regression can be used to evaluate the performance of factors at different return quantile(s) which further improves the accuracy and robustness of stock selection strategies, especially on the percentage of stocks with highest (or lowest) factor values to invest. In addition, with so many factors exist, an extensible platform based on python is proposed to perform factor analysis with quantile regression capability. The platform is designed, implemented, and validated for stocks in the Taiwan stock market.

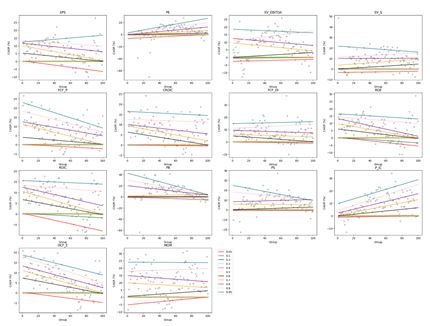

The experimental results show that choosing the quantile with the largest impact coefficient appearing on the tail of head of quantile regression analysis can significantly improve the return rate of the investment portfolio and reduce risk. The proposed and implemented platform not only complete the designated works but also improve the efficiency of Python-based stock strategies backtesting using the Cython conversion as detailed in this work.

Finally, this study uses data from the Taiwan stock market over the past 20 years for backtesting, verifying the effectiveness of the proposed platform and strategy.

Downloads

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Chihcheng Hsu, Haoping Liu

This work is licensed under a Creative Commons Attribution 4.0 International License.